| << Chapter < Page | Chapter >> Page > |

Although the process by which a monopolistic competitor makes decisions about quantity and price is similar to the way in which a monopolist makes such decisions, two differences are worth remembering. First, although both a monopolist and a monopolistic competitor face downward-sloping demand curves, the monopolist’s perceived demand curve is the market demand curve, while the perceived demand curve for a monopolistic competitor is based on the extent of its product differentiation and how many competitors it faces. Second, a monopolist is surrounded by barriers to entry and need not fear entry, but a monopolistic competitor who earns profits must expect the entry of firms with similar, but differentiated, products.

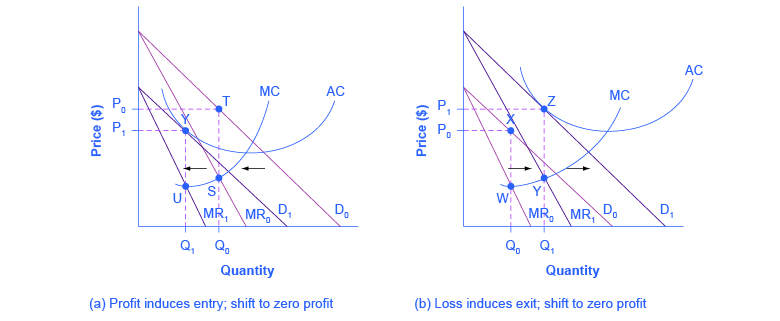

If one monopolistic competitor earns positive economic profits, other firms will be tempted to enter the market. A gas station with a great location must worry that other gas stations might open across the street or down the road—and perhaps the new gas stations will sell coffee or have a carwash or some other attraction to lure customers. A successful restaurant with a unique barbecue sauce must be concerned that other restaurants will try to copy the sauce or offer their own unique recipes. A laundry detergent with a great reputation for quality must be concerned that other competitors may seek to build their own reputations.

The entry of other firms into the same general market (like gas, restaurants, or detergent) shifts the demand curve faced by a monopolistically competitive firm. As more firms enter the market, the quantity demanded at a given price for any particular firm will decline, and the firm’s perceived demand curve will shift to the left. As a firm’s perceived demand curve shifts to the left, its marginal revenue curve will shift to the left, too. The shift in marginal revenue will change the profit-maximizing quantity that the firm chooses to produce, since marginal revenue will then equal marginal cost at a lower quantity.

[link] (a) shows a situation in which a monopolistic competitor was earning a profit with its original perceived demand curve (D 0 ). The intersection of the marginal revenue curve (MR 0 ) and marginal cost curve (MC) occurs at point S, corresponding to quantity Q 0 , which is associated on the demand curve at point T with price P 0 . The combination of price P 0 and quantity Q 0 lies above the average cost curve, which shows that the firm is earning positive economic profits.

Notification Switch

Would you like to follow the 'Microeconomics' conversation and receive update notifications?

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|